SBA Franchise Growth: Why the SBA 7(a) and 504 Programs Are a Franchisee’s Best Friend

SBA Franchise Growth: Why the SBA 7(a) and 504 Programs Are a Franchisee’s Best Friend

Franchising is projected to exceed $920 billion in economic output in 2026, with nearly 845,000 units and 8.9 million jobs nationwide. Despite headlines about economic slowdown and credit tightening, the franchise sector is expanding — and smart operators are using SBA 7(a) and SBA 504 loans as strategic growth tools.

If you’re a current or aspiring franchisee, understanding how these SBA programs work could be the difference between owning one unit… and building a multi-unit platform.

The Franchise Sector Is Growing—Even in a Tight Economy

Key 2026 Franchise Outlook Data:

Projected output: $920+ billion

Estimated establishments: ~845,000 units

Employment: 8.9 million jobs

19% of franchisees control nearly 60% of total units

Franchising isn’t collapsing—it’s recalibrating. Growth is shifting toward disciplined operators in essential service sectors like:

Child services

Commercial and residential services

Health and wellness

Value-based retail

Why does this matter?

Because banks prefer structured, proven systems in uncertain markets. Franchise brands offer historical performance data, national marketing support, vendor purchasing power, and operational systems—making them inherently more “lendable” than independent startups.

And that’s where SBA financing becomes powerful.

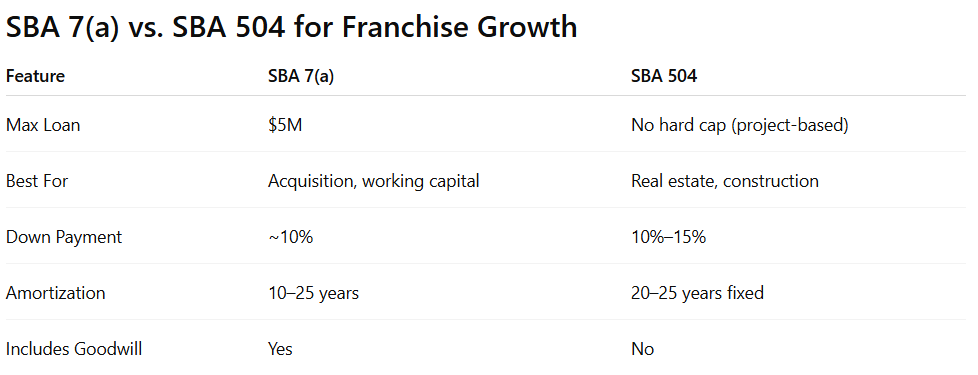

What Is the SBA 7(a) Loan for Franchises?

The U.S. Small Business Administration 7(a) loan program is the most common SBA loan used by franchisees.

SBA 7(a) Highlights

Up to $5 million in total financing

10-year term for business acquisitions

25-year term if real estate is included

As little as 10% equity injection

Can finance goodwill, equipment, working capital, and franchise fees

The 7(a) program is ideal for:

Buying an existing franchise location

Launching a new franchise unit

Acquiring multiple units

Partner buyouts

Refinancing higher-cost debt

Because lenders understand franchise models, especially brands listed in the SBA Franchise Directory, approvals can be faster and more structured than traditional conventional loans.

What Is the SBA 504 Loan for Franchise Real Estate?

The U.S. Small Business Administration 504 loan program is designed specifically for owner-occupied commercial real estate and heavy equipment.

SBA 504 Highlights

10% down payment (sometimes 15% for startups or special-use properties)

20–25 year fixed-rate financing on the SBA portion

Can finance land, construction, or building purchases

Structured as 50% bank / 40% SBA / 10% borrower

The 504 program works extremely well for:

Franchise restaurants buying their building

Hotel franchise construction

Childcare center facilities

Medical or wellness franchise properties

If you’re building a long-term, multi-unit franchise strategy, owning your real estate through a 504 loan can dramatically increase enterprise value.

Why the SBA 7(a) and 504 Programs Are a Franchisee’s Best Friend

Let’s break this down strategically.

1. Lower Capital Requirements

Instead of 25–35% down required by many conventional lenders, SBA programs often require:

10% equity injection

Flexible collateral structure

Longer amortizations

That preserves liquidity—critical in tight credit cycles.

2. Longer Terms = Stronger Cash Flow

10-year amortization on goodwill (7a)

25-year amortization when real estate is included

Fixed-rate 20–25 years on 504 SBA portion

Lower monthly payments increase:

DSCR strength

Expansion capacity

Multi-unit scalability

3. Banks Favor Franchise Systems

In tight lending environments, predictability wins.

Franchises provide:

Historical performance data

Standardized operating systems

Brand-level marketing

Vendor purchasing power

This predictability reduces perceived lender risk.

4. Fuel for Multi-Unit Expansion

Remember this data point:

Approximately 19% of franchisees control nearly 60% of total units

That means ownership is professionalizing.

The operators winning in 2026 are:

Installing GMs early

Building SOP-driven infrastructure

Leveraging centralized accounting

Scaling geographically in high-growth states like Texas, Florida, Arizona, and North Carolina

SBA financing allows disciplined expansion—not reckless growth.

SBA Construction Loans: The Complete 2026 Guide to Ground-Up & Owner-Occupied Projects

Most people misunderstand SBA construction loans—including a lot of bankers.

How to Qualify for an SBA Franchise Loan

While exact criteria vary by lender, most SBA franchise borrowers need:

Credit score: 680+ preferred

10% liquidity injection

Global cash flow support (if multi-entity)

Relevant management or industry experience

Post-closing liquidity reserves

In 2026, lenders are requiring deeper documentation and stronger liquidity positions.

Borrowers who maintain W2 income while launching semi-absentee franchises are often viewed more favorably.

SBA 7(a) vs. SBA 504 for Franchise Growth

Smart Strategy:

Many growing franchisees use both programs:

7(a) to acquire or expand operations

504 to purchase the property

This combination improves long-term asset control and EBITDA stability.

Larger Franchise Transactions & SBA Pari Passu Financing

For transactions exceeding SBA limits, lenders sometimes structure pari passu financing, where:

The SBA portion remains within program limits

A conventional loan is layered alongside

Risk is shared proportionally

This structure is common in:

Multi-unit franchise roll-ups

Portfolio acquisitions

Larger hospitality transactions

It allows franchisees to scale beyond $5 million in total capitalization while still leveraging SBA support.

Real Example: Disciplined Growth with SBA Financing

A multi-unit commercial cleaning franchise operator:

Purchased first unit using SBA 7(a)

Installed GM and documented SOPs

Stabilized margins over 24 months

Acquired second unit within same territory

Centralized accounting and recruiting

By year four, they controlled five units — with layered management .

That’s not hustle. That’s structured leverage. And SBA financing made it possible.

Why Franchising Is Structurally Attractive Right Now

Franchises are outperforming because of:

National purchasing power

Centralized marketing support

Unified technology stacks and AI integration

Access to structured lending programs

Add in demographic migration trends toward the Southeast and Southwest , and you have a clear expansion map.

Need-based sectors continue outperforming discretionary businesses.

The opportunity isn’t speculative. It’s system-driven.

Final Thoughts: Structure Wins in 2026

Franchising crossing $920 billion in projected output is not hype—it’s a structural signal.

The operators who win will:

Choose essential service brands

Maintain liquidity discipline

Use SBA 7(a) for operational growth

Use SBA 504 for real estate control

Install management layers early

Expand strategically — not emotionally

If you’re serious about franchise growth, the SBA isn’t just a lender.

It’s your capital partner.

And in a market that rewards discipline over speculation, the 7(a) and 504 programs may be your best friend.