SBA Ground-Up Construction Loans for Franchise Systems

Build, scale, and own your franchise locations with low down payments, long-term financing, and SBA-backed construction solutions.

SBA ground-up construction loans for franchise systems allow entrepreneurs and multi-unit operators to finance the development of new, from-scratch locations using SBA-backed programs like the 7(a) and 504 loans—often with as little as 10–15% down and long repayment terms.

These loans are ideal for franchise brands expanding into new markets or building custom locations tailored to brand specifications.

What Are SBA Ground-Up Construction Loans for Franchise Systems?

Financing used to build a new franchise location from the ground up

Typically backed by SBA 7(a) or SBA 504 loan programs

Covers:

Land acquisition

Site development

Construction costs

Equipment and buildout

Long-term financing (up to 25 years)

Lower down payments than conventional construction loans

SBA ground-up construction loans are designed to reduce risk for lenders while giving franchise operators access to affordable capital. Unlike traditional construction loans that often require 25–35% down, SBA loans significantly lower the barrier to entry for qualified borrowers.

Why Franchise Ground-Up Construction Is a High-Opportunity Investment

Proven business models reduce operational risk

Brand recognition drives faster customer acquisition

Scalable expansion for multi-unit operators

Real estate ownership builds long-term equity

Custom-built locations maximize efficiency and branding

Franchise systems—especially in sectors like quick-service restaurants (QSR), fitness, hospitality, and healthcare—are expanding aggressively. Ground-up construction allows operators to secure prime locations and build to exact brand specifications, which can significantly improve long-term profitability.

For example, brands like fast-casual restaurants or drive-thru concepts often require specific layouts that only new construction can provide.

How SBA Ground-Up Construction Loans Work

SBA 7(a) Construction Loans

Up to $5 million total loan size

Can finance:

Land purchase

Construction

Equipment

Working capital

Single loan structure (construction → permanent financing)

Variable or fixed interest rates

SBA 504 Construction Loans

Designed for owner-occupied real estate

Structure:

50% bank loan

40% CDC (Certified Development Company)

10% borrower down payment (can be 15–20% for startups)

Long-term fixed rates on CDC portion

Ideal for larger, real estate-heavy franchise projects

Both programs can be used for ground-up construction, but the choice depends on deal size, use of funds, and borrower profile.

How to Qualify for SBA Ground-Up Construction Loans

Credit score: Typically 680+

Down payment:

10% (existing operators)

15–20% (new franchisees or startups)

Franchise approval: Must be listed in the SBA Franchise Directory

Experience:

Prior business or industry experience preferred

Multi-unit franchise experience is a major advantage

Financials:

Strong personal financial statement

Liquidity reserves

Business plan:

Construction timeline

Cost breakdown

Revenue projections

Lenders also evaluate the strength of the franchise brand, location viability, and contractor experience.

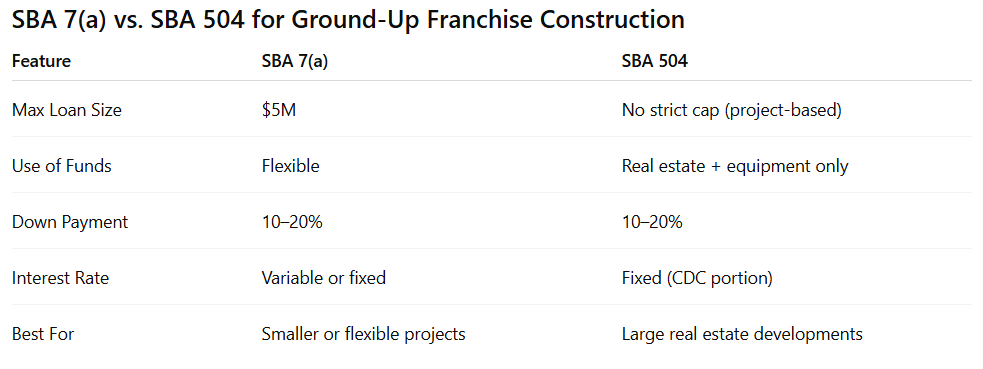

SBA 7(a) vs. SBA 504 for Ground-Up Franchise Construction

Key Insight:

Use SBA 7(a) if you need flexibility (working capital, soft costs). Use SBA 504 if your project is heavily focused on real estate and you want long-term fixed rates.

SBA Pari Passu Financing for Larger Franchise Construction Deals

Used for projects exceeding SBA loan limits

Structure:

SBA loan + conventional loan sharing equal lien position (“pari passu”)

Enables:

Larger developments

Multi-unit builds

Portfolio expansion

For example, a franchise developer building multiple locations simultaneously may combine SBA financing with conventional debt to scale faster while maintaining favorable terms.

Real-World Use Case

A multi-unit franchisee in the quick-service restaurant space wants to build a new drive-thru location:

Total project cost: $3.2 million

Structure:

SBA 504 loan covers 40% ($1.28M)

Bank finances 50% ($1.6M)

Borrower injects 10% ($320K)

Outcome:

Fixed-rate financing on a large portion of the project

Lower cash requirement than conventional financing

Long-term asset ownership

This structure allows the operator to preserve capital while expanding aggressively.

Benefits of SBA Ground-Up Construction Loans for Franchise Systems

Lower equity requirement compared to traditional loans

Long repayment terms improve cash flow

Access to larger projects with structured financing

Supports rapid multi-unit expansion

Build-to-spec construction enhances operational efficiency

These advantages make SBA loans one of the most powerful tools for franchise growth.

Challenges to Consider

Longer approval timelines (60–90+ days)

Detailed documentation requirements

Construction risk (delays, cost overruns)

SBA eligibility rules must be strictly followed

Working with an experienced SBA lender or advisor is critical to navigating these complexities.

Conclusion: Is an SBA Ground-Up Construction Loan Right for Your Franchise?

SBA ground-up construction loans are one of the most effective ways to finance new franchise locations with favorable terms, lower down payments, and long-term stability. Whether you’re launching your first unit or scaling a multi-unit portfolio, these loans provide the capital structure needed to grow strategically.

If you’re planning to build a franchise location from the ground up, now is the time to explore SBA financing options and structure your deal for maximum leverage and long-term success.

Call to Action

Ready to build your next franchise location?

Get pre-qualified for an SBA construction loan

Evaluate whether SBA 7(a) or 504 is best for your project

Structure your deal for optimal leverage and scalability

Contact an SBA lending specialist today to start your project.